We use cookies to enhance your experience. Basic cookies are essential for the proper working of this website. For example, they save your language preferences. They also help us gather anonymous information about the use of our site. More information in our Cookie Policy.

Studying in university: a profitable investment

It is said that knowledge takes up no space and yet deciding to pursue university studies can take up a big chunk out of family finances. Aside from the fact that a labor market might be able to absorb more or less skilled labor, we should look at the question of whether or not to pay for higher education from an investment point of view: is it profitable to attend university? And if yes, which one and for how long?

First things first: why should you go to university?

As with any other kind of investment, your decision should be justified and have a clearly defined objective. To decide why you want to study in university when you’re 17 years old is very difficult – most of us did not know what we really wanted to do or be in the future.

The answer to this question can take many forms. It is important, with the help of family, to stay clear of “reasons” that are not relevant and would actually endanger the investment, such as:

- Because all my friends are going

- Just because…

- Because I’m the best in my class and it would be weird not to pursue higher studies… what would my family say?

- Because I want a successful professional career

Taking up university studies is a major life decision that will shape many things to come and so the answer must be carefully reasoned and future proof, such as:

- Because I would like to exercise a regulated profession for which a university title is needed (e.g. lawyer or surgeon)

- Because I want to be eligible for positions that require a university degree

- Because I want to follow my passion (e.g. architect or professor)

Investment rationale behind your university studies

Once the objective behind the investment in university is defined, we need to calculate the profitability of the studies and the institution where they will be carried out. As in any other investment analysis, we will look at the income and expenses related to the transaction. To make things simpler for our example, I have chosen a case of university studies during 4 years for a student that does not work during this time and has no state aid. The reference costs I’ve taken from publications in the internet and I have rounded them off – you should adapt the calculation to your own specific case!

Our sample investment would look something like this:

- Yearly tuition cost: 10,000 euros / year

- Yearly cost of living (university housing, groceries, transportation, leisure…): 12,000 euros /year

- Opportunity cost (time): 23,000 euros / year

Please note that these costs will vary depending on which school and city you choose for your studies. You can adapt the exercise easily for your own situation.

Please note also that the cost of living is relevant whether you study living at home or away. Also, we have added the opportunity cost of the time spent studying (and thus not generating revenue).

For the purpose of simplicity, the expenses are supposed constant throughout the 4 years and are spread equally over the 12 months of the year.

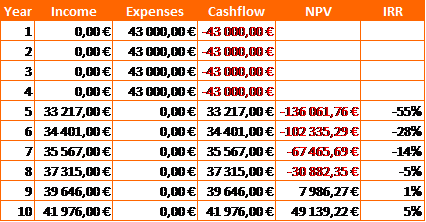

- Years 1 – 4: 0 euros

- Year 5: 33,217 euros / year (gross salary c. 40,000 euros)

- Year 6: 34,401 euros / year (gross salary c. 42,000 euros)

- Year 7: 35,567 euros / year (gross salary c. 44,000 euros)

- Year 8: 37,315 euros / year (gross salary c. 47,000 euros)

- Year 9: 39,646 euros / year (gross salary c. 51,000 euros)

- Year 10: 41,976 euros / year (gross salary c. 55,000 euros)

As stated above, we assume there is no income during the studying period. Thereafter, we assume a gross salary that increases linearly (for the purpose of this exercise) based on a professional improvement due to accumulated experience over time. No break in the professional life is taken into account for this exercise.

With these data we can set up the table below, where we calculate our cashflow and look at the NPV (Net Present Value) and the IRR (Internal Rate of Return) to evaluate our investment:

Based on the result of the NPV and using a discount rate (value of money) of 2% we observe that, based on our assumptions, the payback of our investment happens after 9 years.

But of course if the starting date of employment were later, or if the salary were lower than budgeted above, the payback period would be longer. Additionally, if the expenses were larger than assumed (private university, need to retake courses, or other), the investment would have a poorer yield. Nowadays it’s easy to calculate different scenarios with tools like Excel® or similar, that integrate the formulas for NPV and IRR.

So, is the investment needed worth it?

The example above shows clearly that going to university demands a considerable effort from an investor’s point of view, which is only worth doing in certain cases. It is important to monetize as soon as possible the knowledge and skills acquired, be it through third-party or self-employment.

An alternative to “better suffer” the financial effort is to work while studying. The job will probably be hard and pay little, but the idea is to acquire as much first-hand experience as possible.

The question of which university to attend is important as tuitions differ greatly and depending on the school or college we’ll not only “buy” the education but also access to its network of business relationships and their job exchange. It is not uncommon that by paying more for your studies you will access employment that will pay more also, which in turn renders your initial investment more profitable.

Maybe we should all change our mindset and, the same way we go to our bank with a project in mind and discuss the expected profit and loss of our business idea, and the ups and downs of buying our dream house, once children are nearing the end of high school they would sit down with their parents and discuss their life project: what they have decided and why, how much money they need and how they expect to earn it back. Then we would have profitable investments.

11/2021

-

How do investment funds work?

Investment funds are baskets of securities chosen because of their growth prospects by asset management companies that are experts in financial markets. These funds work on a co-ownership basis: when you invest in a fund, you acquire ownership that corresponds to a share of a basket of equities or bonds already selected and actively managed by experts. This means investing in funds can feel safer than buying individual securities, particularly for a novice. Moreover, investment funds tend to have variable capital, which allows you to trade in your securities on a secondary market at any given moment. The funds can take several legal forms, such as the Société d’Investissement à Capital Variable (SICAV) and the Fonds Commun de Placement (FCP). There are three broad categories of fund: passively managed investment funds, actively managed investment funds and hedge funds.

-

Incentives and assistance to boost Luxembourg entrepreneurs

The government is increasingly keen to attract entrepreneurs to Luxembourg as well as to nurture entrepreneurial ambitions among the country’s residents - and is providing financial incentives and other forms of assistance to encourage them.

-

Investing in rental property in Luxembourg: a good idea?

You want to invest in a property in the Grand Duchy and then make a rental? At first sight, it seems an excellent decision! Investing in a rental property remains attractive, especially in a country where the market for rented residential real estate continues to display a high potential.